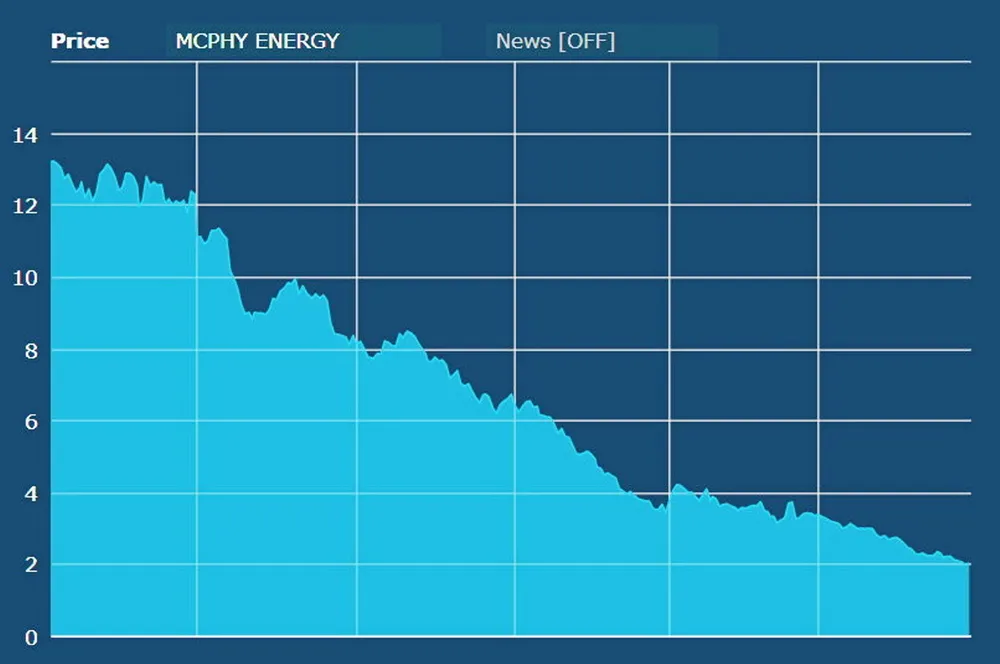

ANALYSIS | Hydrogen electrolyser makers standing firm amid a quintuple whammy of pressures

Share prices continue to fall amid slower-than-expected roll-out of subsidies and outside threats, writes Leigh Collins ahead of the World Electrolysis Congress