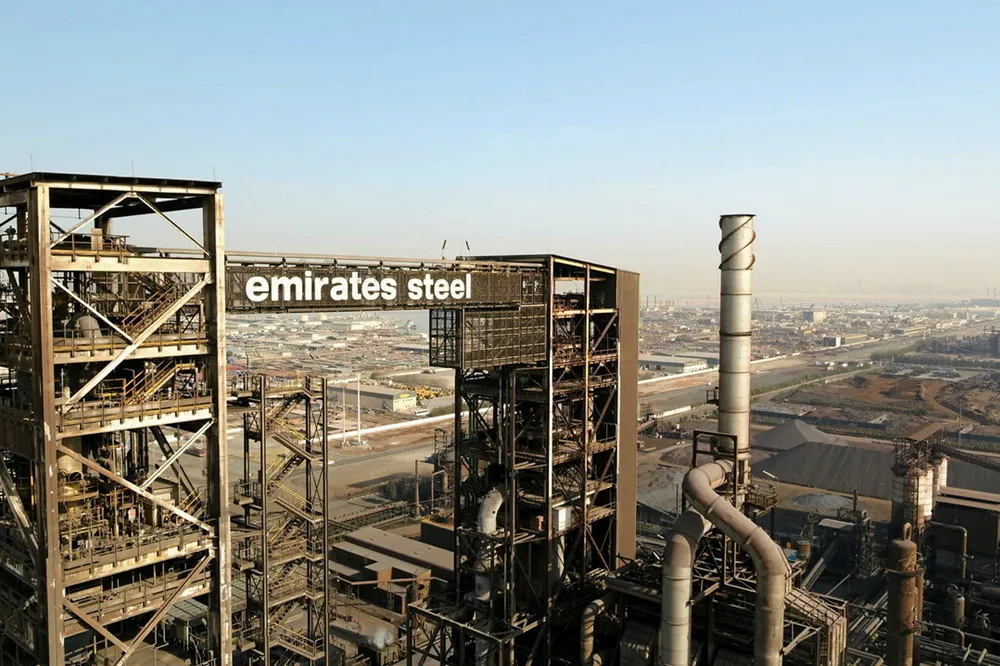

MENA nations 'should export direct-reduced iron made with green hydrogen, rather than the H2 itself': think tank

Replacing fossil gas used in existing direct-reduced iron production facilities could make more commercial sense than shipping hydrogen directly